WESTERN DIGITAL: THE FUTURE OF HARD DRIVES IN THE ERA OF ARTIFICIAL INTELLIGENCE

- Mar 6, 2025

- 3 min read

Western Digital (WDC) is somewhat overshadowed by everything related to cloud computing and artificial intelligence. But let’s be honest: what is wrong with a solid piece of hardware? All that data has to be stored somewhere. We would like to introduce one of the new major positions in our fund.

Artificial intelligence as a catalyst for HDD market growth

The growth of artificial intelligence and data centers is dramatically increasing demand for high-capacity storage. Hard disk drives (HDDs) remain the dominant solution for storing massive volumes of data thanks to their cost efficiency and scalability, with 80% of cloud data still stored on hard drives.

WDC management itself recently presented HDD market forecasts for shareholders, showing how AI is expected to catalyze massive growth in data creation and the related demand for data storage. WDC CEO Irving Tan spoke about future hard drive technologies, including HAMR technology.

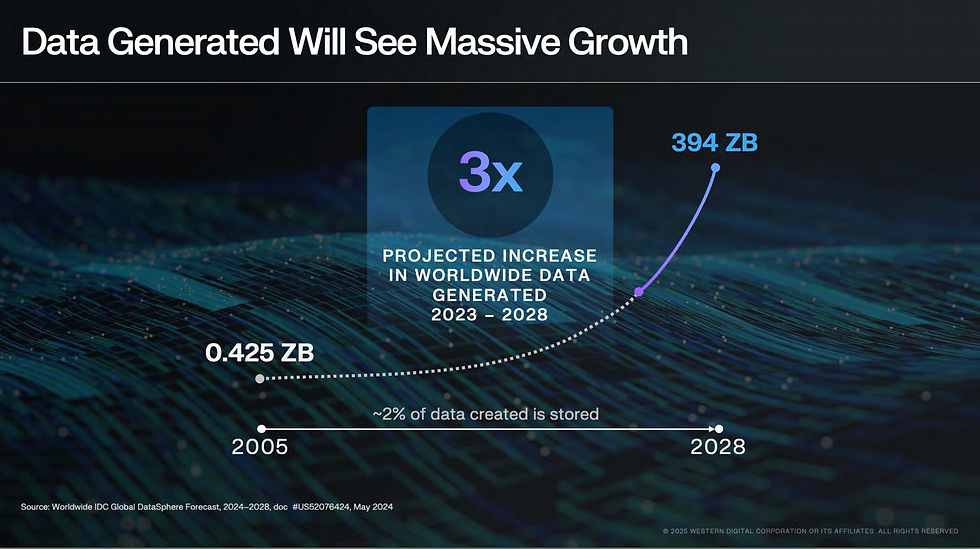

In Tan’s presentation, WDC forecast that by 2028, 394 ZB of data will be generated annually and installed cloud storage capacity will grow at a rate of 23%. Artificial intelligence using text, images, and video will require enormous amounts of cost-efficient data storage, leading to increased demand for digital storage in data centers, with an expected 131% increase between 2024 and 2028.

WDC stated that thanks to the transition to HAMR and other advanced technologies, it expects to maintain storage costs per TB that are 6x lower than flash memory between 2024 and 2030. It also stated that the total upfront and operating costs of hard drives are 3.6x lower than flash-based storage in a standard hyperscale data center.

In addition to announcing its move toward HAMR hard drives, WDC is also exploring new growth opportunities through the development of hard drives, as well as potential AI computing technologies and DNA and optical storage technologies.

A smart undervalued bet in an oligopolistic market

WDC is expected to benefit from the above-mentioned trends over the long term thanks to its strong position in an oligopolistic market, where together with Seagate, both companies each hold approximately a 40% market share in the HDD market. Following the decline in HDD demand in 2022–2023, both WDC and Seagate rationalized capacity, which led to stronger pricing discipline and gross margin growth above 38% in recent quarters. This trend, together with long-term contracts, indicates lower cyclicality in the industry and more stable returns.

Following the February spin-off of SanDisk (formerly WDC’s NAND division), WDC is now traded as a standalone company. However, after the separation, WDC remains temporarily undervalued until the market fully reflects its real value. This is also reflected in the valuation of its main competitor Seagate, which trades at a premium of more than 20% compared to WDC, despite both companies generating almost identical revenues and profits.

We believe this valuation gap will close over the next several quarters, and WDC shares will trade at the same valuation multiples as Seagate shares. The separation of the HDD division from the NAND segment provided investors with a clearer structure, allowing for fairer valuation compared to competitors. In addition, as Western Digital shareholders, we should receive the company’s first dividend as early as June 2025.

Combined with the long-term growth potential of the HDD segment driven by artificial intelligence, this represents an investment opportunity we cannot afford to miss.

For the above reasons, we have included Western Digital shares in the portfolios of both sub-funds, with a one-year target price of USD 60 per share, which, at the current share price of USD 42, implies a return of more than 40%.

We will present more detailed information about this opportunity to our investors during our regular quarterly webinar.

Thank you all for your trust.

The STARTEEPO Team

Disclaimer

The information contained in this article was prepared by STARTEEPO s.r.o., with its registered office at Plynarni 1617/10, Prague (“the Company”), which is the 100% shareholder of STARTEEPO Invest, investiční fond s proměnným základním kapitálem, a.s. The Company draws information from reliable sources and has exercised reasonable care to ensure that the information is not false or misleading; however, it does not guarantee its accuracy in any way. This material is intended solely for promotional purposes and does not replace the fund’s prospectus. It is intended as preliminary information and does not replace professional advice on financial investments or comprehensive risk disclosure. The information provided herein does not constitute an offer or solicitation to buy or sell financial instruments. Investment decisions may only be made based on the current version of the fund’s articles of association. Past performance is no guarantee of future results. This document has been prepared with due care and attention; however, the company makes no guarantees regarding its accuracy, correctness, timeliness, or completeness. The content of this document is protected under copyright law; the company is the copyright holder. The Company is not liable for the dissemination or publication of information by third parties.

Comments